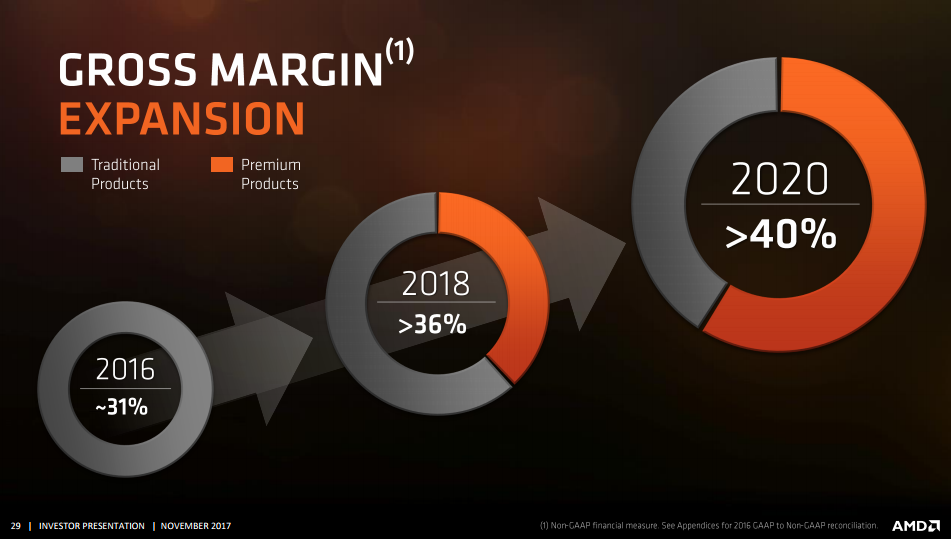

AMD currently Running gross margin in the 33-35% range, reporting a 35% margin in 3Q17

AMD currently Running gross margin in the 33-35% range, reporting a 35% margin in 3Q17

On the Gross Margin Expansion, AMD seems to be on track for management’s 2018 gross margin projection of 36% in 2018, and 40% by 2020. With sales set to grow as a result of EPYC deployment along with their other product lines and success stories like the Intel deal that is a stamp of approval for AMD’s technology. Any sort of friendship for Amd that shares the Intel market or Sale is good for AMD now. Advanced Micro Devices, Inc. may have some huge upside soon ahead if not in q4 2017 probably in q1 or q2 2018. And investors have a rival company to thank to, Intel. The new deal the AMD announced, new semi-custom deal with Intel. Canaccord Genuity maintains a Buy rating and $20 price target for AMD’s stock. Intel will now be using AMD’s Vega GPU in its multi-chip high-end notebook packages. Every body could guess who is the loser here, Nvidia. Nvidia has already called the deal a losing deal and probably they mean for Intel that instead of traditionally working with Nvidia decided to go with AMD. For AMD increasing gross margins should translate into more room for R&D, leaving space for a healthy profit.

“As such, we reiterate our positive thesis on AMD which is further underwritten by management’s ability to monetize the portfolio as strong near-term crypto-currency GPU demand, stronger Ryzen sales and first Ryzen Mobile launches should alleviate risks in Q4/17,” Canaccord Genuity’s Matthew Ramsay wrote.

“while H2/18 sets up as an inflection point with our industry checks indicating 7nm chip development timelines remain intact for what should prove even stronger CPU products across AMD’s roadmap versus Intel during 2H/18 and 2019.” Canaccord Genuity’s Matthew Ramsay.

AMD currently operates at a gross margin in the 33-35% range, reporting a 35% margin in 3Q17:

Gross margin was 35%, up 4 percentage points year-over-year, primarily driven by the benefit of IP-related revenue and a richer mix from the Computing and Graphics segment, which were partially offset by costs associated with our global foundries wafer supply agreement for wafers purchased at another foundry. We continue to make good progress on the ramp of our new high-performance products, which had a positive impact on our gross margins. – Source: 3Q17 Earnings Call

Additionally, on the topic of IP-related revenue, management noted that:When we look at it going forward, we have a pipeline of IP deals and we’re constantly looking at them. And from our standpoint, we’re working several deals in progress. So we believe that IP-related revenue will be a factor as we go forward, but our primary focus is on the product-related revenue and the product-related growth. – Source: 3Q17 Earnings Call

Tags: Technology, AMD, amd stocks, amd value, amd gross margin expansion, amd gross margin, amd increasing value, amd future investing, amd growth

CONTACTS DETAILS &FOR MORE INFO:

https://www.ultragamerz.com/contact/

- Solana Soars: Could a $450+ SOL Ignite a Meme Coin Frenzy? - June 26, 2024

- Rainbow Six Siege – Official Marketplace Trailer - June 25, 2024

- ImagenAI Poised for Takeoff: Can This Ethereum-Based AI Coin Go 20x? - June 25, 2024